Your Teen Already Knows More About Money Than You Think

Your teen calculated the percent change between two data sets last Tuesday. On Wednesday, they analyzed a persuasive text for rhetorical techniques and bias. Thursday, they solved a multi-step equation with real-world constraints.

Then Friday night, they signed up for a free trial they'll forget to cancel, impulse-bought a hoodie through an Instagram ad, and asked you for gas money because "I don't know where it all went."

Those aren't two different teens. That's the same brain — one that already has the analytical tools for every financial decision it'll face, but hasn't been shown that the classroom versions and the real-world versions are the same skill.

This is the gap that April's Financial Literacy Month conversations almost always miss. The internet is about to fill up with "how to teach your teen about money" content — starter budgets, savings jar graphics, compound interest explainers. And most of it will treat financial literacy like a brand-new subject your teen has never encountered.

But your teen isn't starting from zero. They're sitting on a toolkit they've been building since middle school math. Nobody handed them the instruction manual that says: "This is also how money works."

That's what this collection does.

Over the past several months, we've published a series of posts that each connect a specific academic skill your teen is already practicing to a specific financial decision they're already facing. Not theory. Not vocabulary lists. Direct, one-to-one translations between "what you learn in class" and "what you need at the checkout screen, the pay stub, or the tax form."

Together, they form a financial literacy reading path that goes deeper than any single class period or April awareness campaign. You can read them in order, or start with whichever one matches the money moment your family is navigating right now.

The Academic Skills That Are Already Money Skills

Before we get to the reading path, here's the reframe that changes everything: the academic standards your teen is being graded on right now — in math AND in English — are financial literacy standards in disguise.

When their math class asks them to calculate proportional relationships, that's the same skill as reading a pay stub. When ELA asks them to evaluate an author's purpose and identify persuasive techniques, that's the same skill as recognizing why a "4 easy payments of $9.99" button exists. When they interpret data from a table or graph, that's literally what reading a W-2 requires.

The problem has never been that teens lack the skills. It's that nobody has connected the skills they're already practicing to the decisions those skills were designed for.

We wrote about this gap — and what it means now that most states require financial literacy — earlier this year. That post covers the policy landscape: which states require what, where implementation still falls short, and what's still yours to do at home. If you haven't read it yet, it's useful context for everything below.

This reading path picks up where that post leaves off. Instead of "here's what's missing," it's "here's where to start filling it in — using what your teen already knows."

Start With the Moment That Confuses Everyone

→ Understanding Paychecks: What Gets Taken Out and Why

If your teen has income — or is about to — start here.

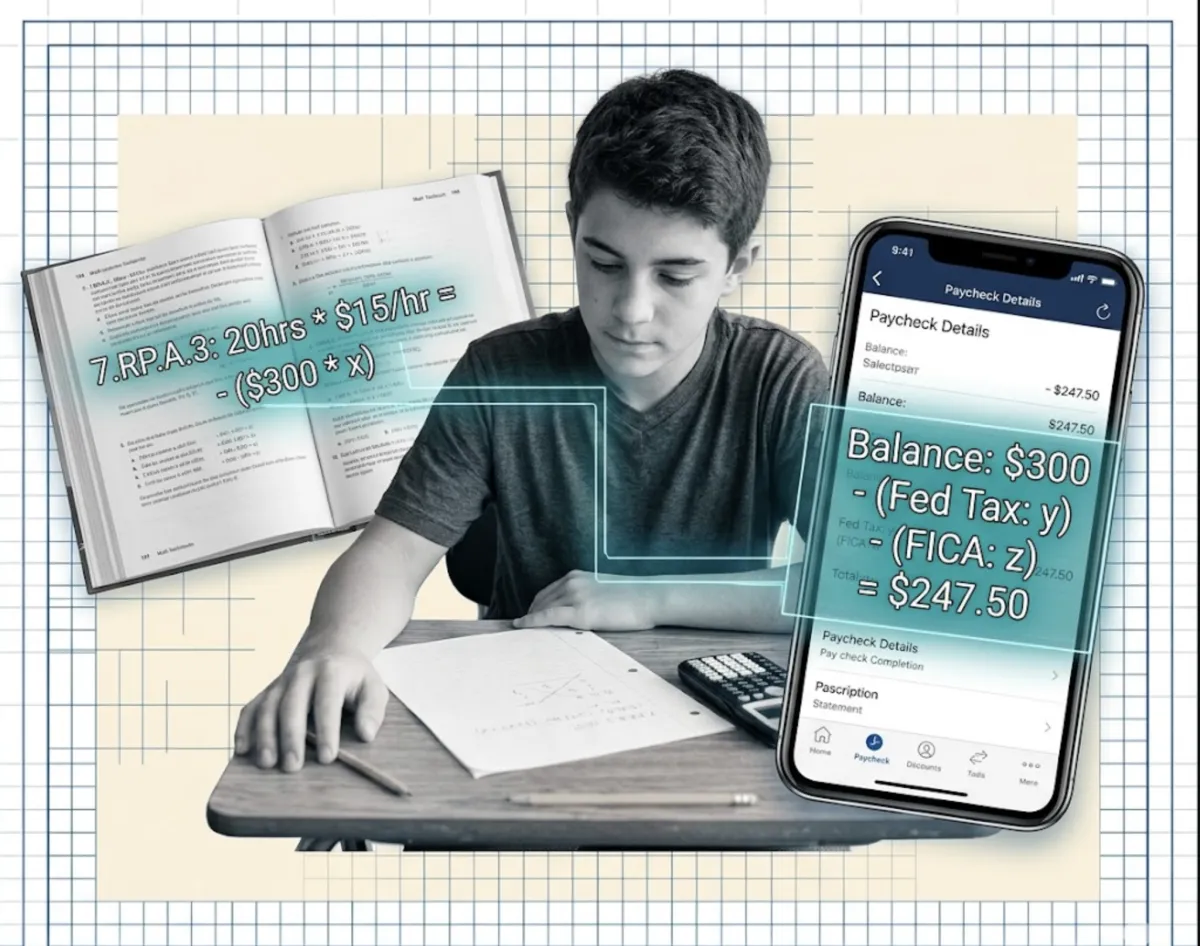

Nothing reveals the gap between "I learned this" and "I can use this" quite like a first paycheck. Twenty hours at $15 an hour equals $300. But the direct deposit says $247. That missing $53 isn't a mistake. It's a series of math problems your teen already knows how to solve — federal withholding, state tax, Social Security, Medicare — all running simultaneously in the background of every single pay period.

This post reframes the pay stub as a word problem. The percentages your teen calculates in class? They're the same percentages on their earnings statement. Proportional reasoning isn't abstract when $53 depends on it.

The academic connection: CCSS Math — proportional relationships (7.RP.A.3), creating equations to model scenarios (HSA-CED.A.1). Your teen's math teacher is already assessing these skills. The paycheck just makes the assessment real.

What you might try at home: Before your teen deposits their next check, sit with the pay stub for five minutes. Not to explain it — to ask: "Can you figure out where each deduction came from?" Let them work the math. The discovery matters more than the explanation.

Then Follow the Money to Tax Season

→ Teen Tax Filing Guide: What You Need to Know First

Once your teen understands what gets taken out of a paycheck, the natural next question is: "Do I get any of that back?" This post answers it — and walks through the tax filing process in a way that connects to skills they've already been building.

Reading a W-2 is data interpretation. Determining whether to file is a conditional logic problem. Understanding the standard deduction versus itemizing is comparing options using numerical evidence. None of this requires learning a new subject. It requires applying math and reading comprehension to a document that actually affects their bank account.

For most working teens, the answer is good news — they're getting money back. That alone is powerful motivation. But the real payoff is the skill: learning to read a government form, follow procedural text, and make a decision based on what the numbers tell you. That's ELA and math working together on something that matters right now.

The academic connection: CCSS ELA — following complex procedural texts (RST.9-10.3), interpreting data presented in tables and forms (RI.9-10.7). CCSS Math — interpreting expressions and solving equations with real-world constraints. Filing a tax return is a literacy task and a math task simultaneously — and your teen's classes have been preparing them for both.

What you might try at home: If your teen worked at all last year, sit with them while they file — or while you walk through the forms together. Don't do it for them. Let them read the W-2 first and tell you what they think each box means. The "aha" moments are where the learning lives.

When the Internet Tries to Outsmart Them

→ Holiday Cash Traps: How Teens Can Spot and Dodge Online Money Pitfalls

This one was written during the holiday spending season, but the threats it covers — buy-now-pay-later traps, subscription auto-renewals, influencer-disguised advertising — aren't seasonal. They're the financial landscape your teen navigates every time they open a screen.

And here's where the ELA connection gets sharp. When your teen identifies that a TikTok Shop ad is using emotional appeal instead of product evidence, they're applying the "ethos, pathos, logos" framework from their English class. When they read Afterpay's terms of service and find the late fee buried in paragraph six, they're doing exactly what their reading comprehension standard demands: evaluating informational text for purpose, audience, and hidden bias.

The English teacher calls it rhetorical analysis. The real world calls it not getting scammed. Same skill, different stakes.

The academic connection: CCSS ELA — determining author's purpose (RI.9-10.6), evaluating reasoning and evidence in arguments (RI.9-10.8), analyzing informational text for credibility. Your teen is already being graded on these skills. Online ads are the informational texts that actually affect their bank account.

What you might try at home: Next time your teen wants to buy something they saw online, don't say no. Say, "Walk me through what the ad is doing." Let them name the persuasive techniques. If they can spot the strategy, they can decide whether to fall for it. That's a fundamentally different conversation than "you can't afford that."

Building the Daily Habit

→ 30-Day Money Challenge for Teens: Build SMART Habits That Stick

The first three posts in this path are about understanding — how paychecks work, how taxes work, how marketing works. This one is about doing. The 30-Day SMART Money Challenge takes the awareness those posts build and turns it into a daily practice.

Here's why that matters: a 2025 Junior Achievement survey found that while 45% of high schoolers have now taken a financial literacy class, 43% still believe an 18% interest rate is "manageable." Knowledge without practice doesn't transfer. The 30-Day Challenge bridges that gap by giving teens a specific action every day — small enough to actually complete, real enough to actually matter.

Each daily prompt connects back to an academic skill. Categorizing expenses into percentages IS statistical thinking. Calculating how many small purchases equal a bigger goal IS applied algebra. Tracking spending patterns over time IS data literacy. These aren't additional assignments on top of academics. They're the same skills, applied to their actual life.

What you might try at home: Some teens love a structured 30-day commitment. Others do better starting with a single week and building from there. If your teen thrives with a checklist, hand them the challenge and let them run. If they resist anything that feels like a mandate, pick three or four daily prompts that feel most relevant and start there. The framework matters more than the pace.

Where It All Connects

→ Financial Literacy 2026: What High School Requirements Mean for Teens

This is the post that zooms out. If any of the above made you think, "Wait — isn't this what school is supposed to cover?" — this post answers that question honestly. Thirty states now require some form of financial literacy for graduation. That's real momentum. And it still isn't enough.

Not because the courses are bad — but because a single semester of vocabulary and worksheets can't replicate the experience of reading your own pay stub, filing your own tax return, or recognizing a BNPL trap in the wild. The state requirements post lays out what's covered, what varies wildly between states, and what's still yours to do at home. It's the "why" behind this entire reading path.

If you started with the other posts and worked your way here, you already have the practical toolkit. This post gives you the big picture — and the confidence that filling in the gaps isn't adding to your teen's plate. It's activating what they already carry.

The Piece That Ties It All Together

Here's what runs through every post in this collection: your teen is not starting from scratch with money. They're sitting in a classroom building analytical, mathematical, and critical reading skills that were designed to apply to real-world decisions — including financial ones. The bridge between "school skill" and "money skill" is shorter than anyone told you.

That's also why the generic "teach your kids about money" advice that floods the internet every April falls flat. It assumes you need to introduce a whole new subject. You don't. You need to activate the subjects they're already taking. Proportional reasoning becomes paycheck comprehension. Rhetorical analysis becomes ad resistance. Data interpretation becomes tax filing confidence. The vocabulary is different. The thinking is identical.

The Standards to Life™ Framework is built on that bridge. It doesn't add a new subject to your teen's plate. It activates what they're already learning and connects it to the decisions they're already facing. That's the difference between financial literacy as a graduation checkbox and financial literacy as a skill your teen actually uses.

Where to Go From Here

Pick the post that matches your teen's current reality:

→ Already earning money? Start with Understanding Paychecks.

→ Tax season approaching? Start with the Teen Tax Filing Guide.

→ Online spending is the weak spot? Start with Holiday Cash Traps.

→ Ready for a daily framework? Start with the 30-Day SMART Money Challenge.

→ Want the big picture first? Start with Financial Literacy 2026: What the Requirements Mean.

And if you want a structured approach that puts all of these academic-to-life connections into a ready-to-teach sequence — with real-world scenarios, built-in differentiation, and standards alignment already done — the Financial Literacy & Consumer Protection Bundle covers budgeting, credit, investing, and consumer protection in five days. Or start with the free Life Skills Progress Tracker to see where your teen's skills actually stand before diving in.

Your teen already has more financial tools than they realize. This month, help them see it.

STANDARDS ALIGNMENT

This roundup covers content aligned to:

CCSS Math: 7.RP.A.3 (Proportional relationships — paycheck deductions, budgeting ratios), HSA-CED.A.1 (Creating equations to model financial scenarios), HSS-ID.A.1 (Representing data — spending categorization and visual analysis), 6.EE.B.7 (Solving real-world equations)

CCSS ELA: RI.9-10.6 (Determining author's purpose — advertising and marketing analysis), RI.9-10.8 (Evaluating reasoning and evidence — financial product claims), RST.9-10.3 (Following complex procedural texts — tax forms, financial documents), RI.9-10.7 (Interpreting data presented in diverse formats), SL.9-10.1 (Collaborative discussion — family financial conversations)

CASEL: Self-management (impulse control, goal setting, financial planning), Responsible decision-making (analyzing situations, evaluating consequences of spending), Self-awareness (recognizing personal spending patterns and triggers)

NHES: Standard 2 (Analyzing influences on health behaviors — marketing, peer pressure, consumer culture), Standard 5 (Decision-making skills applied to financial wellness), Standard 7 (Practicing health-enhancing behaviors — financial wellbeing as component of overall wellness)

Jump$tart Standards: Spending and Saving, Credit and Debt, Employing and Income, Financial Decision Making